The Kiwi Credit Card – The UPI Powerhouse?

by Creditkeeda

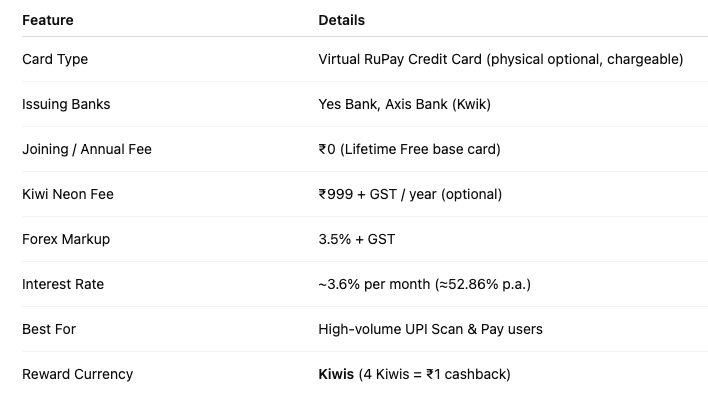

by CreditkeedaThe Kiwi Credit Card, issued via partners like Yes Bank and Au Small Finance Bank, positions itself as India’s first UPI-first credit card, bringing together Scan & Pay convenience with cashback rewards.

However, post multiple devaluations, the introduction of the Kiwi Neon paid membership, and tighter caps, the real question is simple:

👉 Does Kiwi still make financial sense in 2025?

This is a numbers-first, no-fluff review.

Considering an application? Check eligibility and apply here: https://bitli.in/lnKEiiS

At a Glance: Key Statistics

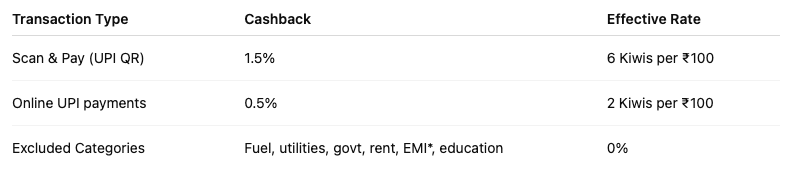

The Rewards Structure (By the Numbers)

The Kiwi card markets itself on "2x Rewards," but you need to look at the effective cashback rate.

⚠️ Critical Reward Calculation Update (Effective 1 June 2025)

Rewards are strictly calculated in multiples of ₹100.

Example:

₹100 → eligible

₹150 → treated as ₹100

₹199 → treated as ₹100

👉 The extra amount earns zero rewards.

This single rule significantly impacts small-ticket UPI transactions.

However, all types of transactions are counted toward milestone spends, even if a portion of the amount does not earn rewards due to rounding.

Base Plan (Free Users)

For Cards Issued After 4 July 2024

* EMI on UPI is eligible, unless covered under no-cost/interest-back offers.

Kiwi Neon Membership (₹999 + GST / year)

Kiwi Neon is not a flat 5% card—it’s a milestone-based accelerator.

Base Neon Benefits

2% cashback on Scan & Pay

0.5% cashback on online UPI

Rewards credited instantly (milestones later)

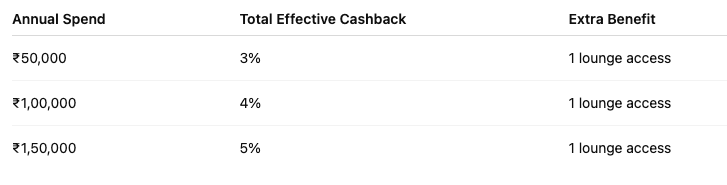

Annual Milestones (UPI spends only)

📌 Important:

Milestone cashback =Target % – cashback already earned during the year

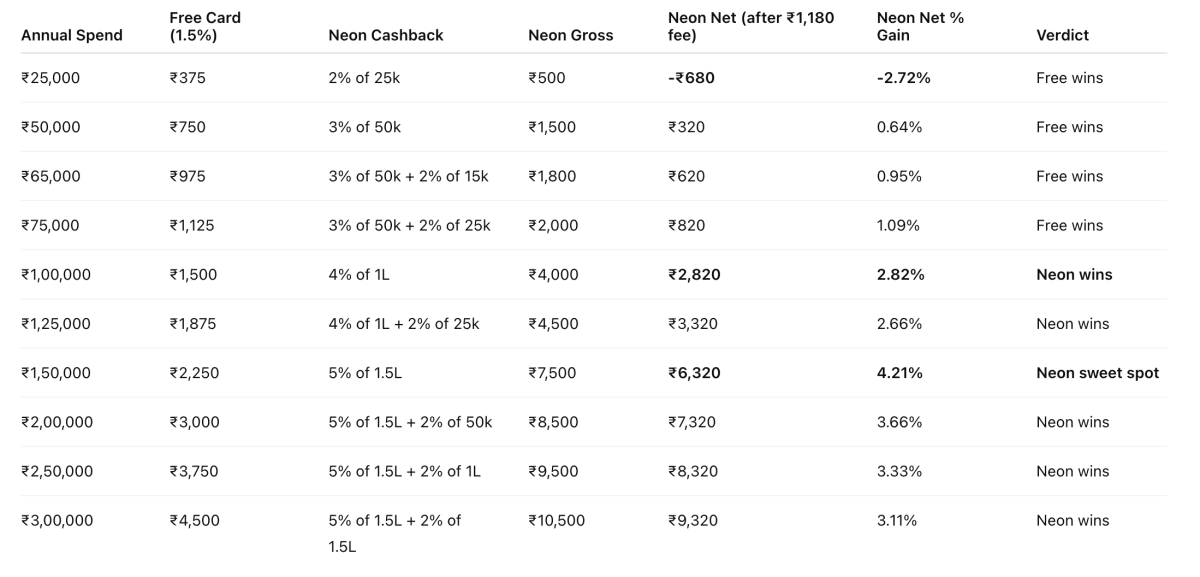

Is Kiwi Neon Actually Worth It? (Math That Matters)

Assumptions

Card issued post 4 July 2024

Eligible UPI Scan & Pay spends only

Free card cashback: 1.5%

Kiwi Neon base cashback: 2%

Milestones: 3% @ ₹50k, 4% @ ₹1L, 5% @ ₹1.5L

Kiwi Neon fee: ₹1,180/year (₹999 + GST)

Cashback Comparison:

🔑 Key Points

Extra cashback applies only after a milestone is fully crossed

Completed slab earns higher %, remaining spend earns base 2%

If your eligible UPI spend is not confidently above ₹1,00,000/year, Kiwi Neon is not worth paying for.

👉 ₹1.5L+ UPI spends: Kiwi Neon becomes market-leading

Kiwi Neon’s peak efficiency is achieved at ₹1.5L, after which returns taper as additional spends earn only the base 2%.

The Biggest Catch: Monthly Reward Cap 🚨

Monthly rewards are capped at 1% of your total credit limit.

Examples:

Credit limit ₹50,000 → maximum ₹500 cashback per month

Credit limit ₹1,00,000 → maximum ₹1,000 cashback per month

This cap applies even to the Neon base cashback.

✅ Milestone cashback is excluded from this cap, which is the only way heavy users extract outsized value.

⚠️ If your credit limit is low, you will never unlock full potential returns, regardless of spend.

Redemption Rules (Often Missed)

Minimum redemption: 500 Kiwis = ₹125

Redemption allowed only in multiples of 500

Cashback is credited directly to your bank account

No vouchers.

No brand lock-in. ✅

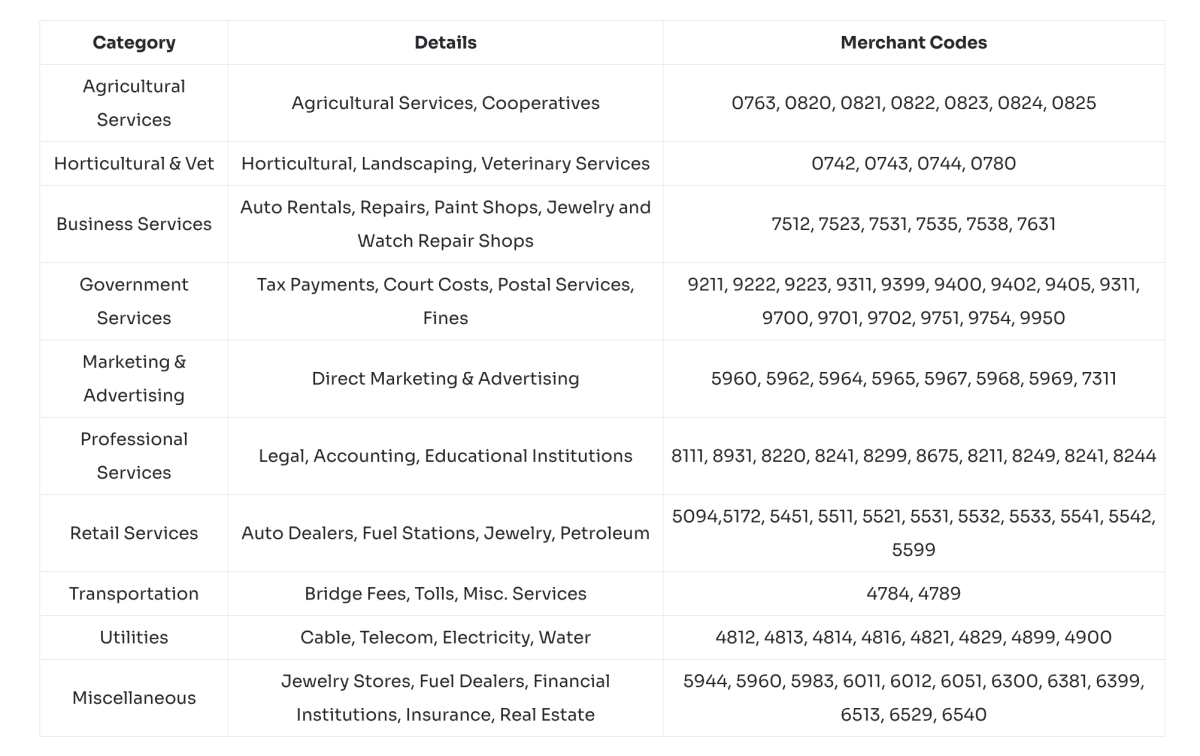

Excluded Categories

The following Merchant Categories will be excluded from the reward

Merchant eligibility is determined by MCC codes received by Kiwi or the issuing bank.

✅ Pros & ❌ Cons

Pros

Lifetime Free base card

Best UPI app UX among credit cards

Direct cashback to bank

Up to 5% effective return with Neon milestones

EMI on UPI earns rewards, very rare feature

Cons

₹100 block calculation hurts small-ticket spends

1% credit-limit-based monthly cap is restrictive

Neon fee makes sense only for high spenders

Confusing issuance across Axis and Yes Bank variants

Online spends earn very little at ~0.5%

Final Verdict

Kiwi is the most rewarding UPI credit card in India only if you are a high-volume Scan & Pay user who can consistently cross ₹1–1.5 lakh in annual UPI spends. For everyone else, the free variant is better and Neon is a costly mistake.

🔗 For readers who find this card suitable, the application link is below:

https://bitli.in/lnKEiiS